When it comes to leaving an IRA to your children, changes to federal law have made things more complicated—and, potentially, more expensive. But there’s a lesser-known estate planning tool that can help preserve the value of your retirement accounts for your children and support charitable causes at the same time: the Charitable Remainder Trust (CRT).

What Changed? The 10-Year Rule

Under the SECURE Act, most adult children who inherit an IRA are considered “non-eligible designated beneficiaries.” This means they must withdraw—and pay income tax on—the entire inherited IRA within 10 years of your death.

For a large IRA, that can mean pushing your child into a higher tax bracket during their prime working years, accelerating tax liability, and losing a significant portion of the account to income taxes.

What Is a Charitable Remainder Trust (CRT)?

A Charitable Remainder Trust is an irrevocable trust that:

- Pays a fixed percentage (e.g., 5%) of its assets annually to a named individual (such as your child) for a term of years or life; and

- Leaves the remaining assets to one or more qualified charities when the trust ends.

Because the trust is irrevocable and eventually benefits a charity, it qualifies for favorable income tax treatment.

When used as the beneficiary of an IRA, a CRT can mimic the “stretch IRA” that was eliminated by the SECURE Act—while also supporting charitable causes you care about.

Real Numbers: Comparing a 10-Year IRA Inheritance vs. a 20-Year CRT

Let’s assume the following scenario:

- You have a $1 million traditional IRA.

- Your child is 47 years old at your death.

- You want to provide for your child while also supporting a charitable cause.

- You name a 20-year, 5% Charitable Remainder Unitrust (CRUT) as the beneficiary of your IRA.

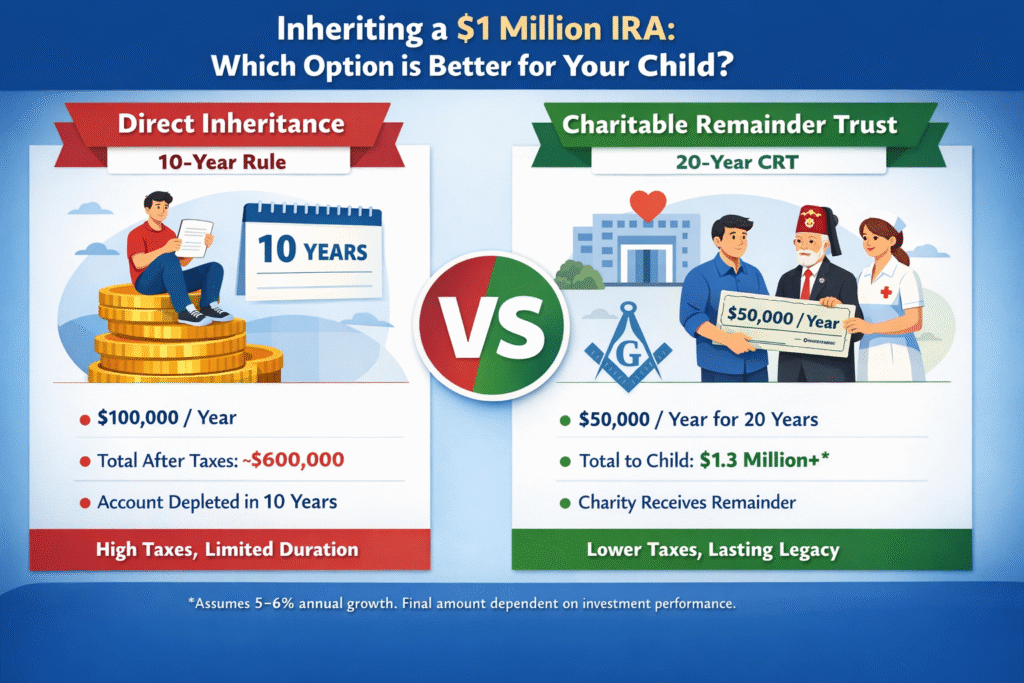

Option 1: Direct Inheritance (10-Year Rule)

Under current law, your child—classified as a Non-Eligible Designated Beneficiary—must withdraw the entire IRA balance within 10 years of your death.

Assuming no investment growth and equal annual distributions:

- Your child would receive $100,000 per year for 10 years.

- Total before-tax distributions: $1,000,000.

Because these withdrawals are treated as ordinary income, they could push your child into a higher federal tax bracket, especially if they already have substantial earned income. It’s not uncommon for these distributions to trigger:

- Top marginal income tax rates (currently 37% federal),

- The Net Investment Income Tax (NIIT) of 3.8%, and

- State income tax, particularly in states like California.

After accounting for federal taxes alone, your child’s after-tax benefit may be reduced to approximately $600,000. Once state income taxes are considered, the net benefit could be even lower.

Option 2: CRT with 5% Payout for 20 Years

With a 5% annual payout over 20 years and 0% growth:

- Your child would receive $50,000/year, for 20 years.

- Total before-tax benefit: $1,000,000—the same principal, spread out over twice as long.

- However, since each payment is smaller, income taxes may be lower each year.

If the trust assets grow at 5–6% annually, which is very realistic with proper investment:

- The child could receive well over $1.3 million over 20 years.

- The charity would also receive a remainder, typically 10% or more of the original IRA.

✅ Result: The child receives more total dollars, spread over time, with more favorable tax treatment—and a charity benefits at the end.

What Kind of Charity?

You can name almost any qualified 501(c)(3) organization, including:

- Your religious or community organization,

- A hospital (like Shriner’s Children’s),

- A cause-oriented nonprofit,

- Or even your local Masonic Lodge (if organized as a nonprofit).

If you don’t have a preferred charity, this is an opportunity to reflect on your values and find an organization that aligns with your legacy.

Why Choose a CRT?

- Tax Efficiency: Spreads income over more years, reducing brackets and taxes.

- Legacy Planning: Supports charitable causes.

- Stretch Alternative: Replaces the “stretch IRA” for non-spouse beneficiaries.

- Customization: Term (up to 20 years) and payout percentage can be tailored.

Important Considerations

- A Charitable Remainder Trust must be properly drafted and administered, especially to comply with IRS requirements for split-interest trusts.

- We use a testamentary CRT, which means the trust is not created until after your death. This eliminates concerns about the irrevocable nature of the trust during your lifetime—you retain full control of your IRA and can change the beneficiary designation at any time.

- The CRT must be named as the beneficiary of your IRA before death; it cannot be added retroactively.

- The trust must include specific provisions to qualify for tax exemption and satisfy the payout and remainder requirements under federal law.

- The trustee (who may be a trusted individual or a professional) will be responsible for trust administration, income distributions, and final charitable payout.

- It’s essential to work with an estate planning attorney experienced in testamentary charitable trusts and IRA beneficiary planning to ensure legal and tax compliance.

Ready to Learn More?

Charitable Remainder Trusts are powerful, flexible tools to balance your desire to provide for your family with your charitable legacy.

If you want to leave your IRA to a child but hate the idea of the 10-year tax crush, a CRT may be the right solution.

We welcome the opportunity to help you explore your options—contact us today to schedule a consultation.

This article is for informational and drafting support purposes only. Consult a qualified California estate planning attorney to assess your specific situation before implementing any strategy. If you live in Kern County, California, you may schedule a free consultation for Estate Planning with Eagle Heritage Law PC. Click here: Book a Consultation.